Financing costs matter

Understanding the full cost picture for residential solar

In the last post, we unpacked the overnight capital costs of a solar PV system. But this was somewhat misleading by omission. Financing costs are another large (and hard to reduce) portion of the solar PV cost structure, even if they aren’t capital costs.

Not only are financing costs large, their recent fluctuations go a long way towards explaining current dynamics in the residential solar market. The slowdown in installations, the shift towards subscriptions and leases, and the bankruptcy of Sunpower are downstream of interest rates as much as seemingly more proximate causes like California’s shift to it’s Net Energy Metering (NEM) 3.0 approach (which reduced payments for energy exports back to the grid).

Financing costs are large

We can see this most clearly with a worked example. Say an independent installer quotes you $3.00 per watt for an 8 kilowatt (kW) rooftop solar system, bringing the overall system costs to $24,000.

If you got a subsidized 0% interest loan1 for the 20-year life of the system, your monthly payments would be ~$100.

At 4% interest, available just a couple years ago for systems secured against the equity in the home, the payments rise to ~$147 per month for a nominal cost across the system life of ~$35,319.

At 8% interest, roughly in line with the last ~12-18 months, payments reach ~$204 per month for a nominal cost of ~$48,889–more than double the overnight capital cost of the system.

Put differently, a system financed at 8% interest is nearly 40% more expensive in nominal terms than one financed with a 4% loan, and more than twice as expensive as one with a subsidized 0% loan.

This matters when nominal 10-year Treasury yields have jumped from ~1.5% at the start of 2022 to a peak at ~4.9% in Q4 2023 and bank prime rates have jumped from ~3.25% to ~8.5% over the same period.

Even bluechip residential solar companies like Sunrun have seen the yields on their securitizations rise from 2.28% in September 2021 to 6.78% in September 2023, for an increase of ~4.5% over the course of 2 years.

These are stiff headwinds which directly impact the cost of residential solar energy for the vast majority of customers who lease or finance their systems.

Solar PV is differentially exposed to rates

Importantly, these financing costs fall harder on solar PV systems.

There are two relevant comparison points here: other generation technologies, and prevailing electricity tariffs from utilities / munis / coops.

At the utility scale, the marginal non-solar watt is coming from wind or combined cycle natural gas turbines (CCGT). In this comparison, solar PV assets have structurally longer duration due to their very low O&M costs. With their moving parts, wind turbines require more maintenance, while CCGTs require both maintenance and ongoing fueling, meaning their costs are relatively more evenly spread across the life of the asset. As a result, the overall cost of solar PV projects is relatively more sensitive to changes in interest rates than alternatives2.

Gas turbines are not realistic options for most homeowners though. For them the relevant reference point is the cost of electricity from their local utility. In this, solar PV has a similar disadvantage, with a larger share of utility tariffs devoted to ongoing operating and capital costs rather than financing costs, buffering the impact of interest rate changes.

As a result, though retail electricity rates have seen steep increases in recent years, those increases have not been on par with the ~30-40%+ increase implied for solar PV by the rise in financing costs.

Cost increases kill marginal projects

Importantly, the rise in financing costs erodes the value proposition for customers.

We can think about the value of a residential solar system as the difference between the cost of the system and the value of the electricity produced—either from self-consumption / avoided electricity tariffs or from export payments.

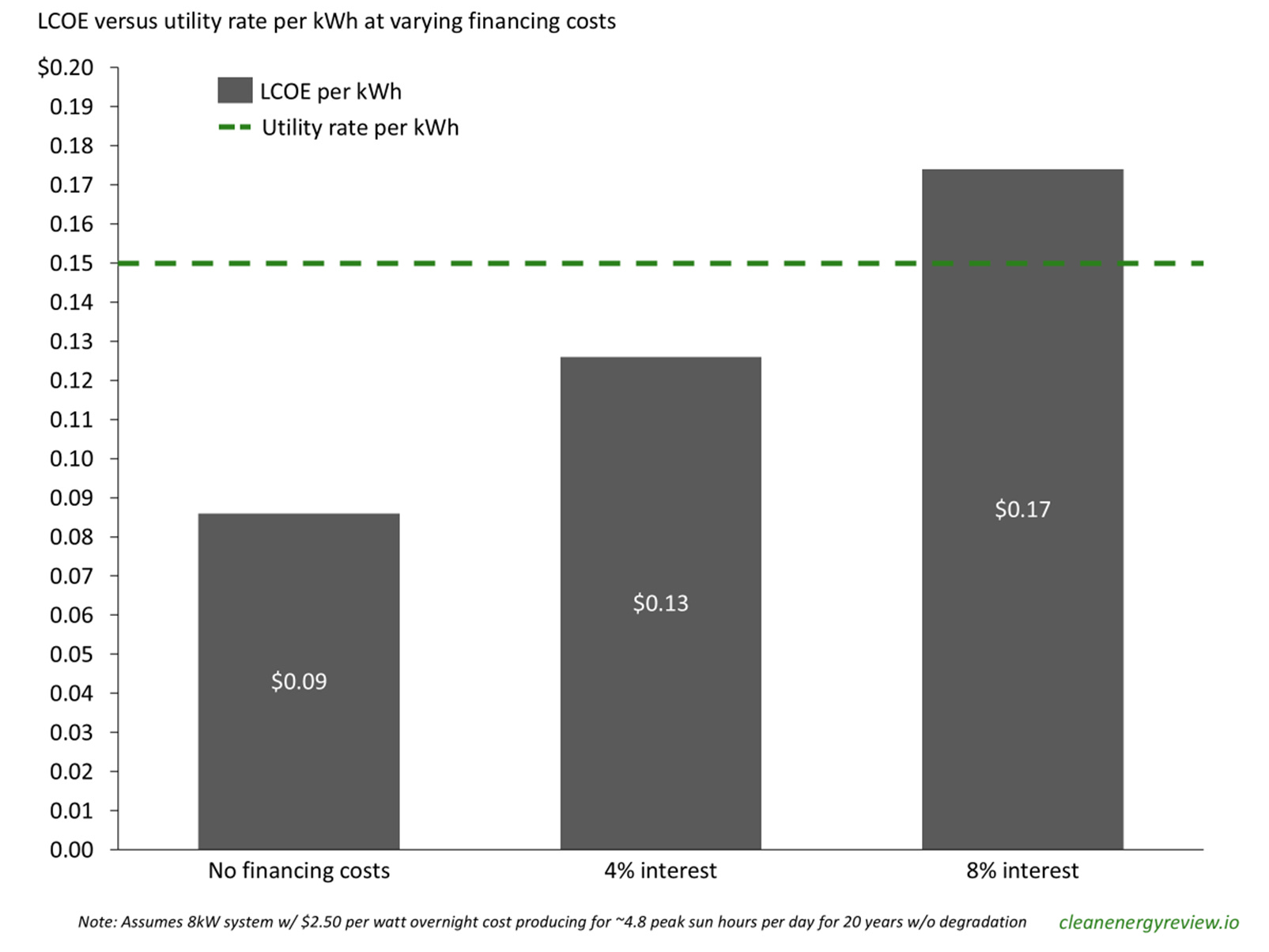

Let’s assume an energy value of ~$0.15 per kWh for our model 8kW system, derived from a combination of avoided utility payments and energy exports. If our 8 kW system achieves a capacity factor of ~20% over 20 years of operation, we get the following ‘levelized cost of energy’ (LCOE) under different financing costs:

A project that made sense at 4% interest rates is distinctly unprofitable at 8%.

The universe of potential solar PV projects can be defined more generally in terms of these same variables: a site’s solar resource (captured here by the capacity factor), a project’s capital costs, its financing costs, and the value of energy produced.

Over the last decade, the decline in capital costs and the rise in utility rates had steadily grown the number of residential solar projects that have positive expected value. The recent sharp rise in financing costs, coupled with the shift towards lower export rates with NEM 3.0 in California, has temporarily reversed this expansion as marginal projects become unviable.

We can see the impacts of both of these effects in the chart below (drawn from this very interest report on the CA residential solar market over the last year):

We see declining installs in Q1/Q2 of 2023 as rates start to rise, a sharp uptick in installs before NEM 3.0 comes into force, then a decline as activity shifts under the new regulatory regime (and continues to be hampered by high financing costs).

Importantly, and seemingly overlooked in the report itself: installs started to decline before NEM 3.0 came into effect, showing how important interest rates were as a driver.

This rate-driven slowdown helped kill Sunpower

At scale, a company like Sunpower or Sunrun or Sunnova can be thought of as a complex machine that identifies positive value projects, convinces customers the projects are worthwhile, installs the necessary equipment, and services both the equipment and the customer for the next 20+ years, all underpinned by a carefully orchestrated financing pipeline.

When market conditions change sharply, this machine can break down.

As the residential solar value prop eroded due to financing cost increases and energy export value reductions from NEM 3.0, it became increasingly important to be able to reshape the customer offering to preserve upside.

This favored companies like Sunrun that had focused heavily on subscriptions rather than outright system sales, and had the capability to sharply ramp up storage attach rate (given the increased value of storage capacity under NEM 3.03). Subscriptions allowed Sunrun to optimize its financing structure on the backend while showing a simple, no-upfront-cost offering to customers. Storage, when integrated with and orchestrated as part of a residential solar system, created significant value for the system as a whole.

These two capabilities could be combined to maintain a compelling customer value proposition and keep the machine running. This advantage has been borne out, with Sunrun reporting sharp increases over the last 18 months in both subscription rates (~78% to ~95%) and storage attachment rates (~18% to ~54%).

Because it relied more heavily on 3rd party financing channels and exposed more of the value complexity to customers, it was harder for Sunpower to reshape its customer value proposition to stay compelling. This left its sizeable customer acquisition and system installation machine running at reduced effectiveness and bleeding cash. When the company ran into issues with its accounting and inventory controls, it lacked the financial flexibility to maneuver and was forced into bankruptcy.

Financing costs are hard to change directly

Unfortunately, despite the importance of financing costs, there are few direct opportunities to drive future savings.

The securitization of residential solar projects is a mature process, as are the tax equity maneuvers that often go along with them. 3rd party financing channels exist, both solar-specific and general, already exist. While future rate cuts will provide a welcome tailwind to the industry, the industry is not in a position to influence this directly.

This leaves developers to focus on reducing upfront costs to drive further value for customers, without neglecting the ongoing importance of financing costs to the overall picture.

There are different ways to structure the loan which I wont’ get into here. For simplicity I am assuming a 20-year fixed rate amortized loan to help isolate the impact of rates on the overall costs of the system.

This is shown quantitatively in Lazard’s latest LCOE report where the steepness of the lines on slide 13 help visualize the implied rate sensitivity. Cost breakdowns by technology are on slide 32-33.